| Retirement Plan |

Type |

Features |

Employee Provident Fund (EPF)

Employee Provident Fund (EPF)

|

Employer-sponsored |

- Mandatory for employees in organizations with 20 or more employees.

- Contributions from both employee (12% of basic salary plus dearness allowance) and employer.

- Tax benefits under Section 80C.

- Tax-exempt interest and withdrawals at retirement age (typically 58 years).

- Guaranteed interest rate announced annually.

- Allows withdrawals for specific purposes.

|

Public Provident Fund (PPF)

Public Provident Fund (PPF)

|

Government-backed savings |

- Open to all individuals.

- Tax benefits under Section 80C.

- Tax-exempt interest and maturity proceeds.

- Lock-in period of 15 years, extendable.

- Flexible contribution amounts.

- Interest rate set by the government.

|

National Pension System (NPS)

National Pension System (NPS)

|

Voluntary, contributory |

- Flexible investment options.

- Tax benefits under Section 80CCD(1), 80CCD(1B), and 80CCD(2).

- Active and auto-choice investment strategies.

- Partial withdrawal allowed for specific purposes.

- Annuity purchase upon retirement for regular pension income.

|

Atal Pension Yojana (APY)

Atal Pension Yojana (APY)

|

Government-backed pension |

- Fixed pension amounts based on contributions and age.

- Government co-contribution for eligible individuals.

- Contributions based on age.

- Safety net for unorganized sector workers.

- Continues until retirement age.

- Pension paid from accumulated corpus.

|

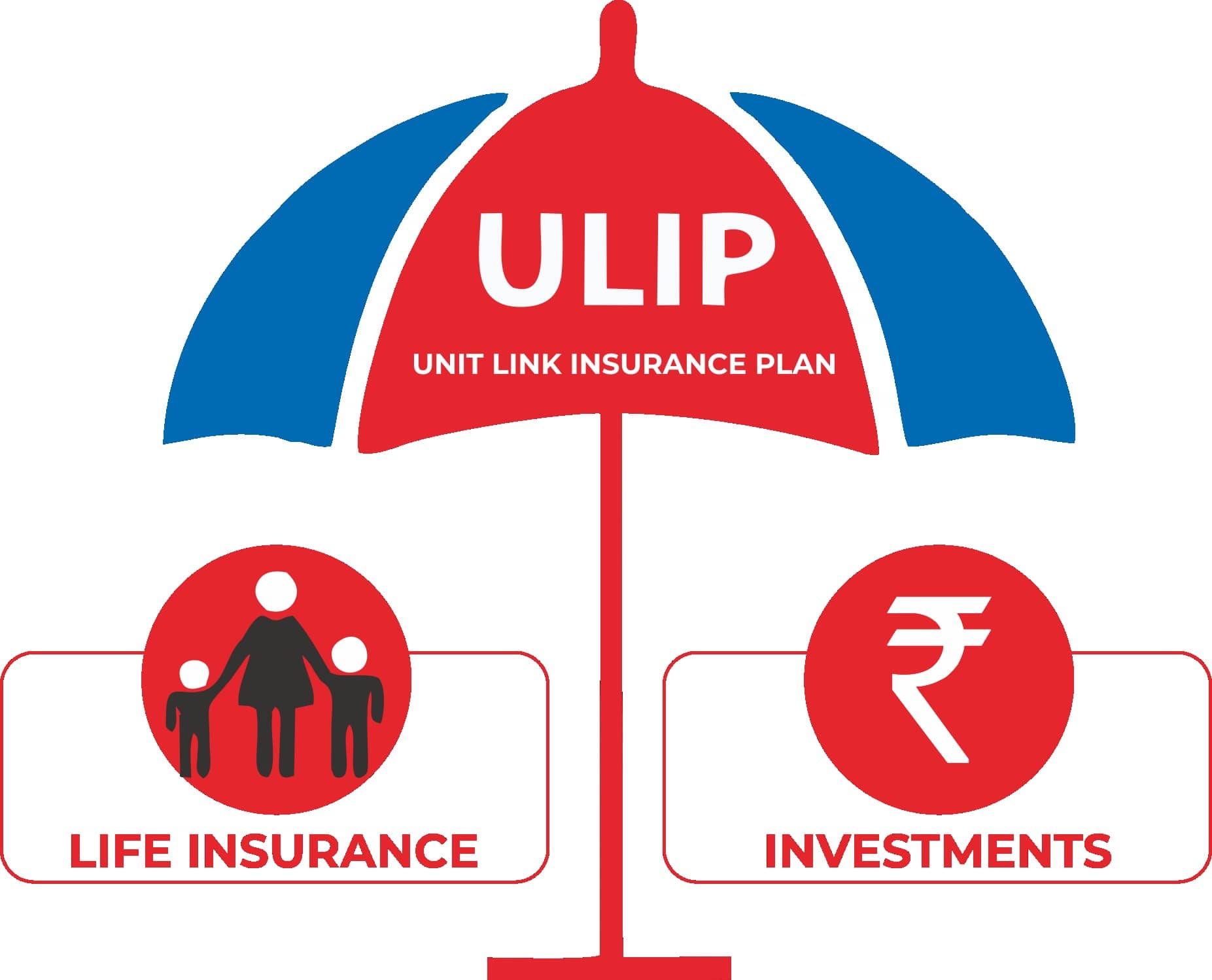

Unit Linked Insurance Plans (ULIPs)

Unit Linked Insurance Plans (ULIPs)

|

Insurance-cum-investment |

- Life insurance coverage with market-linked investment options.

- Tax benefits on premiums and maturity proceeds.

- Flexible fund allocation.

- Death benefit to beneficiaries.

- Loyalty additions, fund boosters, and partial withdrawals available.

|

Senior Citizens' Savings Scheme (SCSS)

Senior Citizens' Savings Scheme (SCSS)

|

Government savings |

- Higher interest rate for senior citizens.

- Tax benefits on investments.

- Lock-in period with quarterly interest payouts.

- Regular income for senior citizens.

|

Mutual Fund Retirement Plans

Mutual Fund Retirement Plans

|

Market-linked investments |

- Potential for higher returns.

- Various fund options: equity-oriented, balanced, debt-oriented.

- Tax benefits under Section 80C for retirement funds.

- Flexible investment amounts and SIP options.

- Long-term wealth creation and risk management.

|